Please join me on Saturday March 2nd between 10 a.m.- 1 p.m. for a complimentary Electronics Recycling event! Please swing by my office located at Windermere Bellevue South 14405 SE 36th Street, Bellevue 98006

Category Archives: Real Estate

4 Questions to Ask Before Selling Your House:

Are you planning on selling your house in 2019? You will no doubt have more than 4 questions on your mind, but knowing the answers to these will get you started with confidence! Let’s get together to answer these and any other questions you may have!

Curious about how much your home is worth in today’s market? Click here for a complimentary home value report: My Home’s Value

Eastside Market Review-Fourth Quarter 2018

The Eastside Market Review is now available for the fourth quarter of 2018.

Read the full report online by clicking the image below.

Real Estate Builds Family Wealth

4 Proven Ways Real Estate Can Build Sizable Family Wealth

Wednesday January 30th, 2019First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers

Recently, David Greene, co-host of the BiggerPockets podcast and a nationally renowned author and speaker, wrote an article in Forbes explaining how investing in real estate could help build wealth. Many of the points he made also apply to a family owning their own home. Here are a few:1. Appreciation

“The rising of home prices over time, is how the majority of wealth is built in real estate. This is the ‘home run’ you hear of when people make a large windfall of money. While prices fluctuate, over the long run real estate values have always gone up, always, and there is no reason to think that is going to change.

One thing to consider when it comes to real estate appreciation affecting your ROI is the fact that appreciation combined with leverage offers huge returns. If you buy a property for $200,000 and it appreciates to $220,000, your property had made you a 10% return. However, you likely didn’t pay cash for the property and instead used the bank’s money. If you consider that you may have put 10% down ($20,000), you actually have doubled your investment, a 100% return.”

2. Leverage

“By nature, real estate is one of the easiest assets to leverage I have ever come across—maybe the easiest. Not only is it easy to leverage the financing of it, but the terms are incredible compared to any other kind of loan. Interest rates are currently below 5%, down payments can be 20% or less, and loans are routinely amortized over 30-year periods.”

3. Paying Off the Debt

“One of the best parts of investing in real estate is the fact that … you’re slowly paying down your loan balance with each payment to the bank… After enough time passes, a good chunk of every payment comes off the loan balance, and wealth is created.”

4. Forced Equity

“Forced equity is a term used to refer to the wealth that is created when an investor does work to a property to make it worth more…

Example of this would be adding a third or fourth bedroom to a property with only two, adding a second bathroom to a property with only one, or adding more square footage to a property with less than the surrounding houses.”

Though Green was talking about investors, the same could be said about a family upgrading their own home.

Bottom Line

Green put it best by saying:

“There are many ways to build wealth in America, but real estate might be the safest, steadiest and simplest way to do so.”

To read the full article, click here.

Eastside Market Review – Fourth Quarter 2017 by Jason E Cook

Fourth Quarter 2017 by Jason E Cook

My Eastside Market Review is now available for the fourth quarter of 2017.

You can read the full report online by clicking the image below.

Another historic year on the Eastsid!

Seattle, Eastside, and King County Real Estate:

Local Market Update – January 2018

2017 closed out the year with historically low inventory and record-breaking price gains. A strong local economy and brisk population growth has helped fuel a steep discrepancy between supply and demand. As long as this imbalance remains, 2018 is on track to remain a very strong seller’s market. For more detailed reports contact #JasonECook #BellevueRealtor

Eastside

2018 Tax Reform & Housing Update

Tax Reform & Housing: A Reference Guide

Disclaimer: This guide is not meant to be a resource for tax advice but instead a resource for basic information concerning only certain aspects of the new tax code and how they may impact the real estate market. You should get tax advice from your accountant or tax preparer who will explain how the entire tax code will affect your personal return.This information comes immediately after the new tax code became law. Some of the information may be revised as the analysis of the new law evolves.

When the tax code was originally being overhauled by the House and the Senate, there were three major proposals being considered that would have substantially impacted the residential real estate market:

- Changing the requirements for the exclusion of gain on the sale of a principal residence

- The reduction on the limit of the Mortgage Interest Deduction (MID)

- The elimination of the State and Local Tax deduction (SALT) which includes property taxes

Let’s look how the tax code has evolved from the original proposal, and decipher what impact experts believe it may have on the housing market.

1. Exclusion of gain on sale of a principal residence

Original Proposal: Owners would need to live in their house for at least 5 out of the last 8 years to claim this exemption. Under the former tax framework, a typical owner, who has lived in their house for at least 2 years out of the last 5 years, would pay nothing in capital gain taxes if they sell the house.

The New Tax Code: No change. The “at least 2 years out of the last 5 years” requirement is unchanged.

Impact on the Market: None.

2. Mortgage Interest Deduction

Original Proposal: Reduce the limit on the mortgage interest deduction (MID) amount from $1,000,000 to $500,000.

The New Tax Code: Reduces limit on deductible mortgage debt to $750,000 for new loans taken out after 12/14/17. Current loans up to $1 million are grandfathered.

Impact on the Market: Assuming a 20% down payment, this reduction in the MID will impact buyers that are purchasing a home between the prices of $938,000 and $1,250,000. Any home under the lower price is still covered and any home over the higher price was not covered under the former tax code either.

What does that mean to the market? Experts disagree. Calculated Risk’s Bill McBride:

“I think the impact of reducing the MID from a maximum of $1 million in mortgage debt to $750 thousand in mortgage debt will have very little impact on the housing market.”

On the other hand, Capital Economics claims:

“The impact on expensive homes could be detrimental, with a limit on the mortgage interest deduction raising taxes for those that itemize.”

3. State and Local Taxes (SALT)

Original Proposal: The elimination of the state and local tax deduction (which includes property taxes).

The New Tax Code: Allows an itemized deduction of up to $10,000 for the total of state and local property taxes and income or sales taxes.

Impact on the Market: Most experts agree that higher taxed regions will be impacted as homeowners in those communities now have a cap on these deductions.

Calculated Risk’s Bill McBride stated:

“SALT will have an impact on housing in some areas. Some people might choose to live in one state over another (if they have a choice), based on taxation. This could impact demand in certain states – especially for the middle and upper-middle class homeowners.”

Mark Zandi of Moody’s Analytics said:

“The impact on house prices is much greater for higher-priced homes, especially in parts of the country where incomes are higher and there are thus a disproportionate number of itemizers, and where homeowners have big mortgages and property tax bills.”

What will be the overall impact on the housing market?

For most of the country, the new tax code will not have a negative impact on the market. As Capital Economics reports:

“Given most households will see an overall tax cut, and potential buyers are likely to put that saving towards their home, we doubt it will have a significant detrimental impact on the housing market.”

There is also no doubt that some higher priced, higher taxed regions will be affected more than others. However, most experts agree that other portions of the tax code will favor the high-end buyer and seller, and this might mitigate many concerns. McBride explains:

“The corporate tax cuts (and other tax cuts) will mostly benefit the wealthy, and this will be a positive for high end real estate.”

What does this all mean to you?

To know for sure, you should sit with your accountant or financial planner and explore how all the aspects of the new code will impact your family.

Most families consider homeownership an essential part of the American Dream, and don’t purchase a home based solely on the tax advantages. The main reasons they buy a home are personal (they just got married, they are looking for a good place to raise children, they want to be near friends and family, they want to better enjoy their retirement, etc.). This will never change.

Looking at the new tax code, Mr. McBride’s opinion makes the most sense:

“There will be some negative impact based on SALT, but overall the impact of these policy changes on housing will be minimal.”

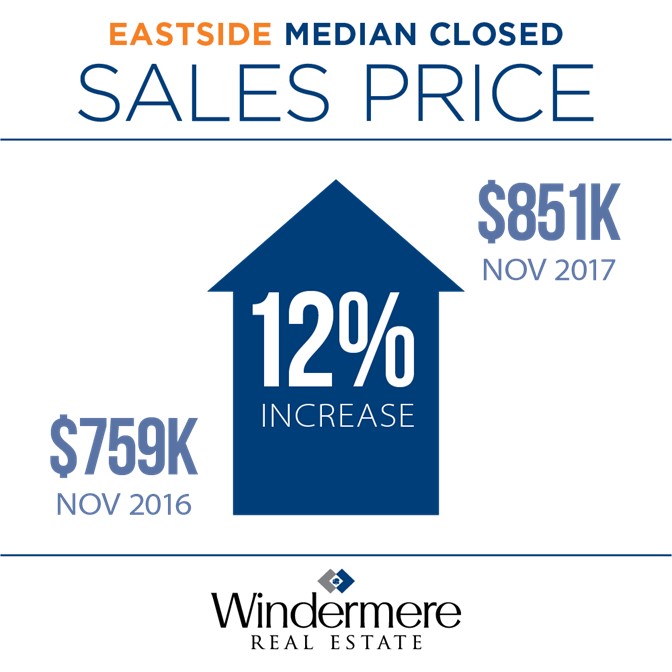

Eastside & Bellevue Real Estate Market Update November 2017

Up 12% compared to 2016EASTSIDE.Residential.And.Condo.November.2017

Seattle Real Estate Home Prices

No “Crash” in sight….

Housing Prices are NOT Heading for Another Crash

As home values continue to increase at levels greater than historic norms, some are concerned that we are heading for another crash like the one we experienced ten years ago. We recently explainedthat the lenient lending standards of the previous decade (which created false demand) no longer exist. But what about prices?

Are prices appreciating at the same rate that they were prior to the crash of 2006-2008? Let’s look at the numbers as reported by Freddie Mac:

The levels of appreciation we have experienced over the last four years aren’t anywhere near the levels that were reached in the four years prior to last decade’s crash.

We must also realize that, to a degree, the current run-up in prices is the market trying to catch up after a crash that dramatically dropped prices for five years.

Bottom Line

Prices are appreciating at levels greater than historic norms. However, we are not at the levels that led to the housing bubble and bust.